Starting out in the stock market sounds like a leap of faith. It conjures up images of screens with red candles, people shouting, "buy now or miss out," and losing money by touching something you don't understand.

And yes, you can lose money. That's part of the deal. But it's also one of the most proven ways to grow your wealth in the long run, especially if you treat it as a real investment and not just a casino with a pretty app.

The idea behind this article is simple: to give you a practical guide to get started from scratch with a clear head. No unnecessary technical jargon. And 15 tips that, if you apply them, will save you from very common mistakes.

First. What does “investing in the stock market” mean (and what doesn't)

Investing is buying assets with the intention that they will grow over time. Time. Years.

It is different from:

- Speculating: entering and exiting quickly, chasing price movements, trying to "guess" the market.

- Gambling: putting money in impulsively, due to FOMO, because of a news story, or because of advice from a stranger.

For a beginner, sensible investing is often boring. And that's a good thing.

A fact that puts things into perspective (and calms you down)

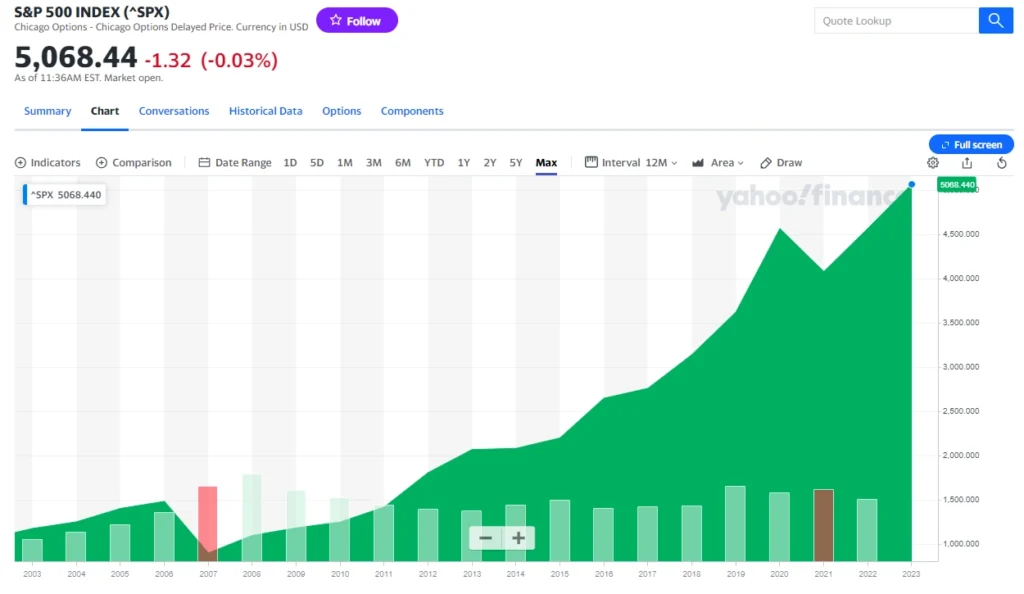

In the long run, equities have been among the most profitable assets. To put it in numbers:

- The S&P 500 (the 500 largest US companies) has grown approximately 10.86% annually since 1957 including dividends.

- Adjusted for inflation, we are talking about around 6.96% per year (also since 1957).

- In October 1957 the index was around 40 points and for October 2025 it is mentioned to be around 6,900 points.

Does that mean he's going to repeat exactly that? No.

Does that mean the stock market always goes up without any surprises? Not really.

This means that, historically, those who have invested long-term, diversified, and with low costs have been much more likely to succeed than those who have tried to juggle multiple investments.

Before investing a penny, take your "profile test" (it only takes 2 minutes)

If you don't know your risk profile, everything else becomes improvisation. And improvisation in the markets has its price.

Take a quick mini mental test:

- If your portfolio drops 20% in a year… do you sleep the same or do you panic?

- How long can you keep the money invested without needing it?

- What is your real goal? (house, retirement, independence, "just to see what happens"...)

- Do you have an emergency fund?

Ideally, you should take a formal profile test (many brokers and robo-advisors offer this). Based on the results, you'll receive an allocation recommendation: more equities if you tolerate volatility, more conservative if you don't.

A practical tip if you're going to request personalized advice: they'll usually ask for your email address to send you the steps and the result. That's fine. But use the result as a guide, not a definitive answer.

1) Define your goal. Without that, there is no strategy

Investing for:

- buy a house in 4 years

- supplement retirement in 25

- building a timeless legacy

Your goal defines your horizon. And the horizon defines how much risk makes sense to take.

Write a sentence. Literally.

“I want to invest X per month for Y years to achieve Z.”.

You're already ahead of the 80% who come in without a plan.

2) Start small. But start

People get stuck waiting for "the perfect moment." Or waiting to have 10,000 euros.

It's not necessary.

Today you can start with small amounts thanks to:

- index funds

- ETFs

- fractional shares (depends on the broker)

If you start with 50 or 100 a month, you're training the habit. And habit is what gives compound interest something to work with.

3) Don't invest money you can't afford to lose

This advice sounds basic, but it is often ignored.

Before investing in the stock market, the reasonable thing to do is usually:

- pay off expensive debts (credit cards, consumer loans)

- set up an emergency fund (3 to 6 months of expenses, as a guideline)

If you invest money that you might need for next month's rent, any downturn will force you to sell at a loss.

4) Assume there will be losses (at some point) and prepare yourself

The stock market is falling. Period.

If your plan only works "if everything goes well," it's not a plan. It's a wish.

It's wise to have an answer to these questions in advance:

- What do I do if my portfolio drops by 30%?

- Am I still contributing?

- Do I have a percentage that makes me lose sleep?

Volatility is not the enemy. The enemy is panic selling.

5) Prioritize equities for the long term (and simplify)

To build wealth in the long term, equities are usually the driving force.

And here's the important part. You don't need any unusual products.

In general, for beginners:

- Yes to indexed/global ETFs

- Yes to a diversified and simple portfolio

- Don't complicate things by doing 18 things at once

6) At first, avoid FOREX, CFDs, and derivatives (if you are starting out)

This needs to be made clear.

FOREX, CFDs, options, futures… are often combined:

- leverage

- complexity

- opaque commissions and spreads

- high probability of error due to lack of experience

You can learn them someday if you're interested. But starting there is like learning to drive a Formula 1 car in the rain.

7) Choose a good broker (reliable and cheap). It really matters

Your broker is your infrastructure. If it's expensive, slow, unclear, or pushes you to trade, that's bad.

What to watch:

- commissions (buying/selling, custody, currency exchange)

- access to ETFs and funds you actually want

- ease of use

- regulation and reputation

- Decent customer service (yes, this matters when there are problems)

Many people, citing quality and cost, often mention Interactive Brokers as a strong option, especially if you want a variety of markets and competitive commissions. But check if it's a good fit for you, your country, your tax situation, and your trading level (their platform can be intimidating at first).

8) If you don't want to complicate things, look at robo-advisors (and compare)

Robo-advisors automate investing based on your profile and goals. They administer a test, propose a portfolio, rebalance it, and you contribute.

In Spain, for example, the following are often cited:

- Indexa Capital

- MyInvestor

Advantages: simplicity, discipline, diversification, automation.

Cons: You pay a commission for the service and give up control over every detail.

To start from scratch, they can be a very reasonable option if what you want is to get started without analysis paralysis.

9) Control your emotions (because the market will test you)

What ruins wallets is usually not a lack of intelligence. It's behavior.

Typical things:

- buy when everything is going up because “this time is different”

- sell when it falls because "it goes to zero"

- change strategy every two weeks

- check your wallet 14 times a day

Practical solution: reduce friction.

- automates contributions

- It limits how much you look at the market

- Write down your plan and review it when you're calm, not in the middle of a fall

HOT TOPICS: WHAT YOU NEED TO KNOW

WHICH ETF SHOULD YOU BUY? DON'T WASTE YOUR TIME WATCHING YOUTUBE… YOUR GURU IS TALKING NONSENSE

Stop guessing. Learn 7 practical filters (costs, index, currency, replication, liquidity, risk) and choose an ETF wisely.

10) Be clear about whether you are investing or speculating (and don't mix them up)

Investing: medium and long term horizon, clear criteria, diversification, low costs.

Speculate: trying to profit in the short term from price movements.

You can do both, but if you do, keep them separate:

- a “serious” long-term part (the largest)

- a small part to experiment with (if you feel like it), assumed as a risk

The classic mistake is to say "I am an investor" and then make decisions like a nervous speculator.

11) Diversify. Don't just "I have 5 stocks"

Diversification is not about having 5 companies from the same country and the same sector.

Diversifying effectively usually involves combining:

- sectors

- geographies

- foreign exchange

- company size

- including asset types (according to profile)

For beginners, an easy way is to use:

- Global ETFs

- global index funds

- Simple combinations like “global + emerging” or “global + small caps”, depending on your plan

Diversification doesn't maximize excitement. It maximizes survival. And that's what allows for growth.

12) Ignore the noise. Seriously. Ignore it

Alarmist news, apocalyptic headlines, videos with thumbnails of fire.

All that sells. But it doesn't help you.

Best sources:

- reports from your ETF/fund manager or provider

- official data

- good books

- consistent educational content (not the kind that thrives on weekly scares)

If your strategy changes because of a single day's news, then it wasn't a strategy.

13) Review and rebalance your portfolio periodically

Not every day. Not every week.

But with a routine, for example:

- every 6 months

- or once a year

Rebalancing is returning to your target distribution.

Simple example: you wanted 80% equities, 20% bonds. If after a year the stock market rises and you end up at 90/10, you sell some of the assets that rose the most or allocate more to the assets that fell short to return to 80/20.

This forces you to do what is emotionally difficult: sell some of the expensive things and buy some of the cheap things.

14) Take taxes into account (because the real return is net)

Investing without considering tax implications is like looking at your gross salary and forgetting what you actually receive.

Things to consider, in general (depends on the country):

- taxation of capital gains

- taxation of dividends (capital gains)

- commissions and withholdings

- if there is a transfer between funds without tax toll (in some places this is key)

Typical basic optimization:

- offset losses with gains when it makes sense

- Defer taxes if you can (postponing payment often helps with compound interest)

If this sounds like gibberish to you, don't worry. Just don't ignore it. Sometimes a seemingly identical product can change significantly due to tax regulations.

15) Get just enough training, but get proper training (and mix theory with practice)

You don't need a master's degree. But you do need a minimum level of education.

Because beginner mistakes cost money. And not a little.

What would I do if I started today?

- Understanding what an ETF is, an index fund, fees, volatility, and diversification

- Learn basic concepts such as expected return vs. risk

- Read 1 or 2 good books on long-term investing

- Start with a simple portfolio and automatic contributions

- fine-tune as you go without changing the plan every month

There are thousands of stock market courses. Choose one that doesn't promise quick returns and focuses heavily on risk management, fees, and psychology. If it only talks about "entries" and "exits," be suspicious.

This is not a personalized recommendation, just a diagram for you to visualize.

- Emergency fund ready.

- Profile test completed.

- Automatic monthly contribution (even if it's small).

- Simple and diversified product (indexed or global ETF).

- Annual review and rebalancing.

And that's it. Yes, "that's it." The hard part isn't designing it. The hard part is maintaining it when the market gets tough.

Typical mistakes to avoid (quick list, to stick on the wall)

- Change your strategy every time there is volatility.

- Buying what's fashionable without understanding it.

- Invest money you'll need soon.

- Paying high fees for pure convenience.

- Use leverage at the beginning.

- Focusing too much on a single action or a single country.

- Looking at your wallet as if it were Instagram.

- Confusing learning with consuming content without taking action.

Getting started in the stock market isn't about finding tricks. It's about doing the basics well, for a long time.

Define your goals. Know your profile. Start small early. Avoid complex products. Choose a good broker or a robo-advisor if you want ease of use. Diversify. Control your emotions. Rebalance your portfolio. And don't forget taxes. Then, keep learning.

If I had to summarize it even further.

Make a plan you can stick to even when you have a bad year. Because you will. And even then, if you stick to it, that's when the long run starts to work in your favor.

My name is Norberto. I've been investing and trading for over a decade. I'm also the author of the Topstep Experience trading course. If you want to learn how to invest and have any questions, feel free to contact me.

You might also be interested in

WHAT ARE THE BEST COURSES FOR INVESTING?

TRADING BROKERS: A GUIDE TO THOSE I USE AND THOSE I WOULDN'T USE

Brokers we would use with our money. Pros/cons and who they are for…

ETFs FOR BEGINNERS: HOW TO BUILD A SIMPLE PORTFOLIO STEP BY STEP

Step by step (without jargon) to assemble a wallet…