If you search for "best broker for trading" on Google or YouTube, you'll see the same thing over and over again.

Bonuses. “0 commissions.” Pretty screenshots of an app. And the typical YouTuber saying that this is the broker he uses with his $800,000 account. Uh-huh. Sure.

The problem is that a broker isn't just any product. It's not like choosing a music subscription. You're choosing where you keep your money, where you execute your orders, what costs you'll incur without realizing it, and what tools you'll have when things get tough (because they always do).

And since you sent me that access error message, let me tell you something important: even when you try to find "good" information, you often run into brick walls, broken links, articles that won't load, or recommendations from influencers who aren't even active. So, perfect. Let's do it without relying on a single link.

This article is about that. About choosing a broker with your head. Without falling for marketing hype.

The broker's advertising doesn't completely lie to you. It only tells you what suits them

A broker can be perfectly legitimate… and still sell you an incomplete story.

Because advertising usually revolves around three things:

- Low or “zero” commissions

- Ease of use (usually the so-called neobrokers with their apps)

- Bonuses or promotions

And yes, it matters. But if you choose based solely on that, you could get into trouble.

For example, “0 commissions” could mean:

- Zero purchase commission, but higher spread.

- Zero commission, but they rip you off on currency exchange.

- Zero commission, but you are not the actual owner of the asset (depending on the product).

- zero commission, but you pay for custody, inactivity, or withdrawal.

Typical. They make it easy for you to get in. As for getting out… you'll see.

Did you come to this article looking for a recommendation and don't feel like reading any further?

I'll make it easy for you…

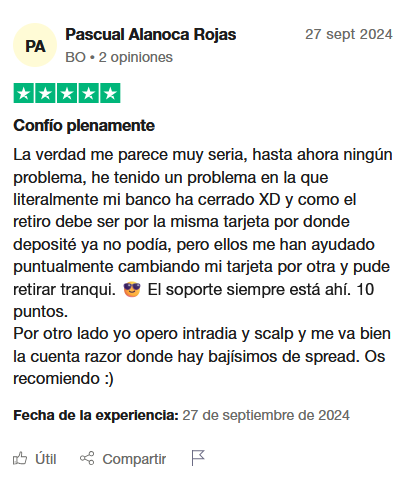

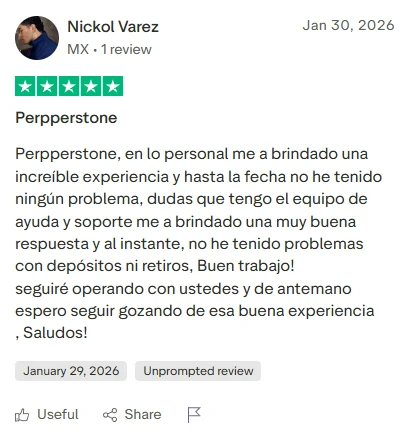

Pepperstone is one of my favorite brokers. Try it and let me know what you think.

- Read reviews and the full Pepperstone review

- More information: www.pepperstone.com

Pepperstone, the traders' opinion

But let's continue…

Step 1: Define what you are going to trade (and how), before looking at brokers

People skip over this. And then come the "it won't let me buy such and such" or "this is a CFD and I didn't want to.".

So first, a mini list:

What do you want to operate on?

- Cash shares (buy and hold, dividends, long term)

- ETFs

- Funds (less common in pure trading brokers)

- Options

- Futures

- Forex

- Crypto

- CFDs (pay attention here)

What style?

- Long-term investment: few transactions per month

- Swing trading: a few trades per week

- Day trading: several per day

- Scalping: many per day, very sensitive to spreads and execution

They're not the same. A broker that's "perfect" for investing in ETFs might be terrible for day trading. And vice versa.

And another thing: if you don't yet know what you're going to do, that's perfectly fine. But then choose a broker that doesn't limit you and doesn't push you towards unusual products just because they're the most profitable for them.

Step 2: Regulation. There's no room for creativity here; it needs to be verified

Regulation is the most basic and most ignored filter for those who are swayed by advertising.

The minimum you want to understand:

1) In which country is the broker regulated?

If you are in Spain, you are usually interested in it being regulated in the EU and operating with a European passport.

Common regulators in Europe:

- CNMV (Spain)

- CySEC (Cyprus)

- BaFin (Germany)

- FCA (United Kingdom, no longer in the EU but still strong)

- AMF (France)

- CONSOB (Italy)

Not everyone has the same reputation, to be honest. But the important thing is that there is real oversight.

2) Is it registered where it claims to be?

This is key: it's not enough for them to just put it on their website. You have to check it with the regulator's registry. And check the legal name, not the fancy business name.

If you're feeling lazy, think about this: you're saving yourself a big headache by checking for five minutes.

3) What protection is there if it goes bankrupt?

In the EU, there is usually a compensation scheme, but it varies by country and institution. Furthermore, cash, custodial assets, and derivatives trading are all different things.

You don't need to memorize it. You just need to read it and understand what it covers and what it doesn't.

Step 3: A "real" broker or a platform that sells you CFDs?

This is where advertising is most deceptive, because they sell you "stock trading" and then you're trading a derivative that replicates the price.

Quick difference

- Cash share: You buy an actual share.

- CFD: Contract for Difference. You don't buy the underlying stock. It's a derivative (not bad, but you should know the difference).

- Options/futures: derivatives too, but with clear rules and specific markets.

I'm not saying CFDs are "bad" by definition (I trade them all the time), but you need to know how to use them because they involve:

- more risk

- default leverage or constant temptation

- less obvious costs (overnight, spreads)

- strong incentives for you to trade more

If your idea is to invest, a broker focused on CFDs may be the wrong place.

A simple question to clarify:

- Do I want to own the asset or just speculate on the price?

Step 4: The actual cost. Not the advertised cost

This is where I would really look closely.

A broker may charge you for:

1) Commission per transaction

The typical one: you buy, you pay X. You sell, you pay X.

But it can also be:

- fixed commission

- commission varies by volume

- minimum commission per transaction

2) Spread

The difference between the buy and sell price. In liquid markets it's small, but with certain products or brokers it can be a silent drain on your profits.

This matters a great deal in:

- forex

- CFDs

- scalping/intraday

- illiquid stocks

3) Currency exchange

If you buy USD shares from a EUR account, many brokers apply the following:

- a currency conversion fee

- or a “worse” exchange rate than the real one (markup)

Sometimes that cost exceeds the buying commission. Seriously.

4) Custody

They charge you for holding positions. Not always, but it happens.

5) Inactivity

If you don't trade for X months, they charge you. And that's ridiculous for a long-term investor.

6) Withdrawals and deposits

- withdrawal by transfer

- Card deposit with commission

- minimum withdrawal fee

7) Market data

In options and futures, or specific markets, there may be subscriptions to real-time data.

The good news: all of this is in the tariff document. The bad news: hardly anyone reads it.

Practical tip: run a simulation of your case.

- “I’m going to buy 1,000 euros worth of a US ETF every month.”

- “I’m going to make 20 trades a month in European stocks.”

- “I’m going to day trade EURUSD”

And calculate it with the broker you're looking at. If you can't calculate it easily, that's a bad sign.

Step 5: Execution and quality. This isn't shown in ads, but it's noticeable when it hurts

If you trade more actively, execution is part of the cost.

Things to look out for:

1) Type of orders

Does it allow:

- limited

- to market

- stop loss

- take profit

- stop limit

- Trailing stop?

If a platform forces you to trade only with the market and little else, it is taking away your control.

2) Slippage

They execute trades at a lower price than expected, especially during periods of high volatility. It happens everywhere, but some brokers handle it better than others.

3) Market hours and access

Can you trade pre-market or after-hours (if needed)? Which exchanges does it cover? Which products?

4) Interruptions

The typical scenario: news day, crazy market, and the app "won't load." If that happens to you and you're leveraged, it can be a disaster.

Reviews are very useful here… but be careful. Reviews on Trustpilot and similar sites are full of:

- People who lost money blame the broker

- affiliates manipulating opinions

- competition by making mudslinging

Even so, if you see a recurring pattern (constant drops, blocked withdrawals, unresponsive support), take it seriously.

Step 6: Custody and ownership of assets. The fine print that almost no one looks at

If you buy stocks or ETFs, you'll want to know:

- Are they in your name, in a segregated account?

- Does the broker lend your shares? (stock lending)

- If he lends them out, can you turn it off?

- What happens to your voting rights?

- How do they manage dividends?

- Can you transfer your portfolio to another broker?

For investment purposes, the possibility of transferring the position is a huge advantage. If you're investing long-term, you don't want to be "stuck" because exiting means selling (and paying taxes, spreads, etc.).

Step 7: Customer service. This seems secondary until you actually need something

Typically, you won't talk to support for months.

And one day:

- Your account is blocked for verification

- There is a problem with an income

- You need a tax certificate

- a dividend doesn't add up

- you want to request an adjustment

At that moment, the broker is the support.

What I would look at:

- Do they have real chat or just bots?

- Do they answer in Spanish if you need it?

- schedule?

- Is there a phone?

- Do they have a decent knowledge base?

And beware of "friendly" support that calls you offering "help" with trading and signals. If they pressure you into using leverage or investing more money, mentally walk away.

Step 8: Taxation and documentation. The boring part that saves you later

If you're in Spain, for example, you'll want to know:

- Do they give you clear reports on capital gains, dividends, and withholdings?

- Do they apply withholding tax on dividends? (and how do they document it)

- Do they provide downloadable extracts?

- Do you have a complete transaction history?

The broker doesn't need to "do the tax return for you," but they do need to give you the information without it being an obstacle course.

If a broker makes things too difficult for you here, it will eventually wear you down. And that weariness often leads to mistakes.

Red flags. Warning signs that advertising tries to cover up

If you see one or more, at least stop:

- Aggressive deposit bonuses, with unusual withdrawal conditions.

- Lots of marketing about “get rich”, “live off trading”, “quick returns”.

- They push you to trade with leverage from minute 1.

- “Zero commissions” but nobody explains where the broker makes his money.

- You can't easily find complete rates.

- Confusing regulation or in opaque jurisdictions.

- Difficulty withdrawing money, or many repeated complaints about withdrawals.

- The platform is too simplistic for the risk it offers (high leverage with game-like buttons).

It's not paranoia. It's a filter.

A simple way to choose without going crazy: a homemade scoring system

If you want something practical, do this. Literally in a note on your phone.

Rate from 1 to 5:

- Regulation and trust: __/5

- Actual cost to my operation: __/5

- Products I need (stocks, ETFs, options…): __/5

- Quality of execution and type of orders: __/5

- Deposits and withdrawals (speed, fees): __/5

- Support and documentation: __/5

- Taxation and reporting: __/5

- Ease of use without sacrificing control: __/5

Then add it up.

And after adding it up, one more step that's worth its weight in gold:

Put in a small amount of money at the beginning and try the "full cycle"

- Deposit

- Buy

- Sell (even if it's a small transaction)

- Withdraw

If a broker passes that test with little money, you can already consider upgrading.

If it fails… you've just saved yourself a problem.

Questions you should ask yourself before making a decision (that almost no one does)

- What happens if I want to change brokers in two years? Can I transfer my broker?

- How much will I actually pay per year with my trading style?

- Am I interested in owning the assets or just speculating?

- If I have a problem with a withdrawal tomorrow, how easy is it to resolve?

- Does this broker profit when I trade more? (many yes) Is it worth it for me to be there?

- Am I choosing based on safety and cost... or on an advertisement?

It sounds a bit harsh, but it's the key question.

Conclusion: Choosing a broker is less about “what cool app” and more about “what structure suits me best.”

Advertising shows you the good stuff: clean interface, operating in two clicks, commissions "from 0".

You have to look at what's not shown in the ad:

- real regulation

- total cost

- product type

- execution

- withdrawals

- reports and taxation

And then, yes. You choose the app you like.

Because if the broker is solid, you'll notice it on calm days… but especially on chaotic days. Those days when the market crashes, or there's volatility, or you're nervous and need everything to work as it should.

That's when you're glad you didn't fall for the advertising.

My name is Norberto. I've been investing and trading for over a decade. I'm also the author of the Topstep Experience trading course. If you want to learn how to invest and have any questions, feel free to contact me.

You might also be interested in

WHAT ARE THE BEST COURSES FOR INVESTING?

TRADING BROKERS: A GUIDE TO THOSE I USE AND THOSE I WOULDN'T USE

Brokers we would use with our money. Pros/cons and who they are for…

WHAT HAPPENED TO MARCELLO ARRAMBIDE'S DAY TRADING ACADEMY (DTA)

Why is this trading academy no longer being talked about?